Disagreeing with folks smarter than me is not a great idea. But then again, I never said I was smart.

Today’s topic is about diversification and why “concentrated” stock investors can be more diversified than you think.

The general thought-process today is that in order to be truly diversified, you need to own hundreds (If not thousands) of stocks.

The main argument comes from this idea of volatility. Academics talk about it relentlessly, but I think Dr. William Bernstein outlines it very well in this old post of his: The 15-Stock Diversification Myth

Now I am not going to bash volatility as a risk measure quite like Buffett and Munger do, but I do want to say a few words on it.

First, volatility measures the movement in the price of a stock (Not it’s fundamentals) over a certain period. Stocks that go up and down a lot (In % terms) have higher volatility than stocks that go up and down smaller % amounts.

Secondly, volatility tends to be a decent way to screen for stocks actually. For example, stocks that exhibit lower volatility tend to be larger companies and are typically found in more defensive sectors such as Consumer Staples, Utilities, some Healthcare, etc.

High volatility stocks tend to be smaller companies and can typically be found in more cyclical sectors like Consumer Discretionary, Materials/Energy, etc.

The trick is that within those components of the market, using just volatility may not be the best way to think about the risks that a business faces.

Lastly, I do think volatility is a good measure for behavioral risk. Stocks that go up and down more than the market tend to be stocks that are harder to hold on to for most people (Including myself). This typically can result in investors selling at a loss. So in a long round about way, it’s not the worst proxy in the world for certain forms of risk.

With all that said, volatility does not directly measure the risk of a business being permanently impaired. And this, for a buy & hold investor, is THE important question.

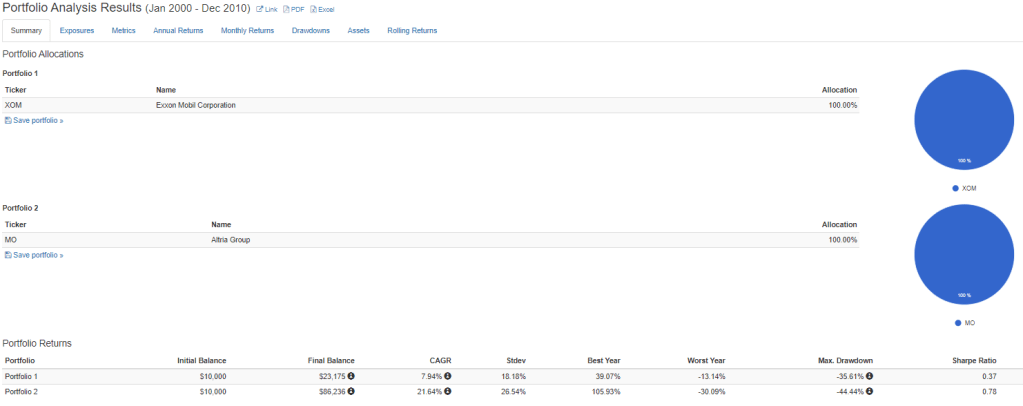

Here is one random example. From 2000-2010 Exxon Mobile had a much lower monthly volatility compared to Altria (About 30% lower):

So, according to many, Exxon is about 30% less risky than Altria. And using volatility, it is, but here are the important questions; Which is the less risky business? What do the fundamentals actually say? What are the economics of each business? Which business is more cyclical or who has more consistent cash-flows? Does either business face disruption from new tech? Etc.

Those are the types of questions to ask from a business perspective.

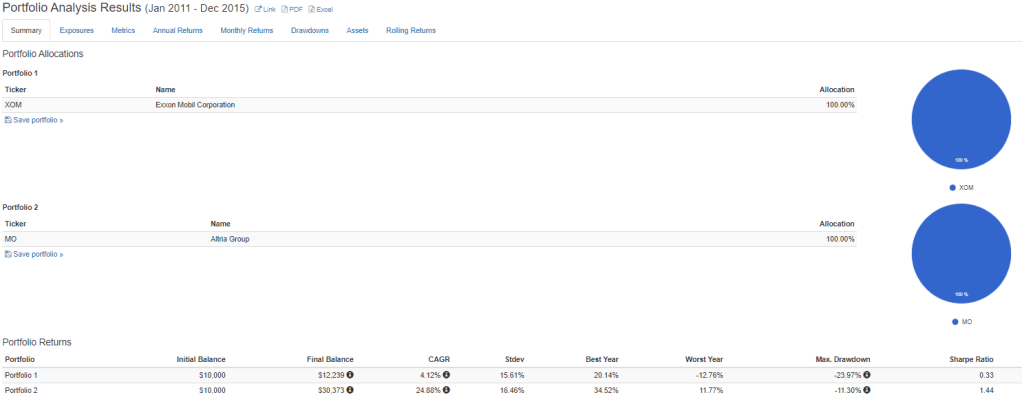

For the record, here is the ensuing decade. Turns out, according to volatility, that Altria was “less risky” in the next 10ish years:

Party Time

Here is another way to think about it in a more abstract way. Say you are at a friend’s wedding. It’s cocktail hour and you start talking to an out of town guest at the bar. After introductions and pleasantries you ask what this person does. They tell you that they help a small number of wealthy families find and invest their money into private businesses.

Well now your curious. What do wealthy families invest in anyways?

Well mostly boring stuff, but right now we have 10 businesses within the “portfolio”:

- Advertising Agency in New York

- Car Dealerships in Georgia

- Auto Parts Stores in Missouri

- Whiskey Distillery in Kentucky

- Multi-Family Housing in Illinois

- Grocery Stores in Ohio

- Food Packaging Company in Ohio

- Home Construction Company in Virginia

- Consulting Firm in California

- Clothing Retail Shops in California

Naturally you ask how often a change is made?

Your new friend mentions that the fund buys (into) or sells (out of) one private company every one to two years. Everything is very slow and as long as the business’ continue to look good when they update their annual figures, changes are rarely made. Upon investment, the families expect to own a stake in these companies for 5-10 years at a minimum. It also helps that most of the business do return some cash profits to us on an annual basis.

One last question before you get back to your date…Do these families invest in anything else? Hedge Funds? Mutual Funds? Anything?

Well yes. Most of the families have about 50% of their investment assets in the private businesses.

Beyond that, all these families keep a separate chunk of liquid assets for rainy day purposes, sleeping well and/or new investments if they come up. A mix of cash, treasuries, and investment grade debt. Nothing fancy. It’s typically around 25% of their investment assets.

Lastly, they also tend to have around 25% in different investments. It depends on the family. Some hold private real estate, others have a mixture of low-cost mutual funds in brokerage or retirement/pension accounts, etc…

Now at first blush, my guess is that you would think those wealthy families were diversified enough in their investments and we’re doing just fine. I know I would. I mean 10 distinct business spread across the entire U.S. All profitable. All with healthy financials. Beyond that, a healthy chunk of safe assets, and another piece in low-cost mutual funds or rental real estate. Sounds pretty nice and low stress actually.

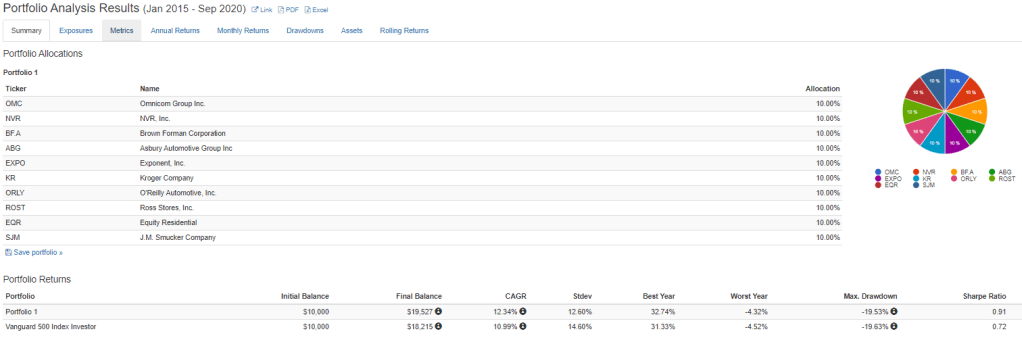

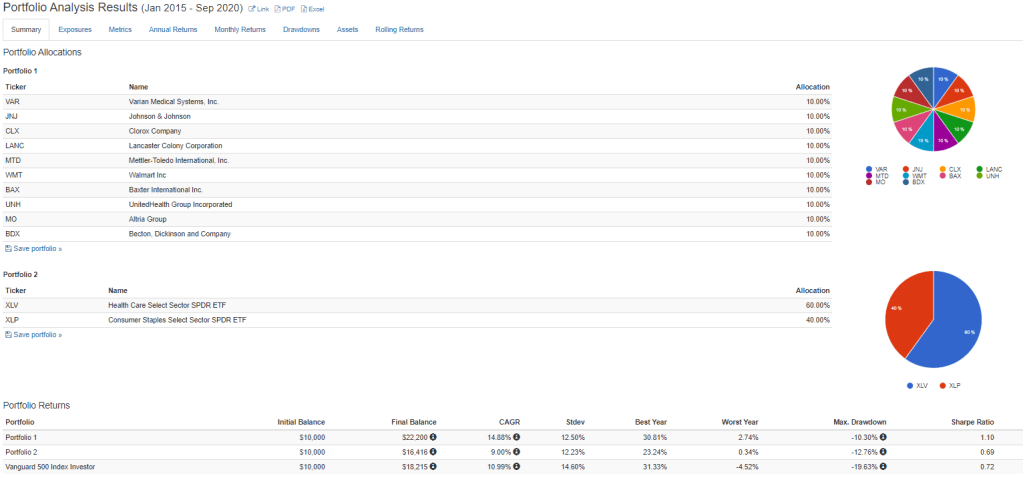

Funny enough, the stock market would agree. Yes, those 10 companies above are actual examples stolen from a list of public companies that rated out as high quality back in 2015:

Now I can hear people screaming “Well sure but you could easily have picked 10 terrible businesses and done horribly”. Kind of true. This is what Dr. Bernstein did in his post which chooses 15 stocks at random.

But here is the catch, you don’t have to pick stocks at random. In fact, you can read the financial history of all public companies. You can read about their industries, their future plans, etc. You can see it all.

Now that does not guarantee you will pick the next Amazon (I would advise against trying to do that anyways), but it does mean you can stick to financially strong companies in easy to understand industries.

My issue with the Bernstein exercise (Not the man himself, who I admire greatly) is that very few people will choose 15 stocks at random. Quick Tip: If you do choose 15 stocks at random, maybe go with the index fund option.

On the other hand, if you choose 15 stocks that have histories of being profitable, have healthy financials, are in mostly defensive or consumer based industries, and are at reasonable valuations, your “risk” picture is going to be very different versus the “monkey throwing darts” approach.

Here is another quick and fun test. Using the same 2015 screen that I used for the above selections, let’s build a random defensive portfolio. Consumer Staples and Health Care. Necessities right?

Okay, so within those two sectors, we will simply choose the 10 stocks ranked the highest in terms of my abbreviated Buffett Score (Quality and Valuation). No discretion, just the highest ranked ones:

What do you know. The 10 stock portfolio has less volatility than the S&P 500 AND much lower drawdown during the panic of early 2020. Also, if you compare it to the sector matched portfolio, it still does better.

Loud Internet Voices

Now let’s move to today’s world. If I were reading through the Bogleheads or WCI forums, and I saw a doctor say they kept 50% of their savings in 10 stocks, 25% is safe assets, and 25% in rental real estate, my guess is that most of the replies would be comments about not being diversified enough in the market.

When the truth is that, this doctor may be perfectly diversified. In fact, the equity positions may be even more defensive than the person with a few equity index funds.

The key of course is what 10 businesses do those 10 stocks represent?

Now, this does not mean I think everyone (Or anyone) should follow this approach. This exercise is purely meant to identify that it is an acceptable approach. And one that has it’s own advantages, both from a risk perspective and a mental perspective.

The baseline, in my opinion, continues to be a globally diversified portfolio of a handful of low-cost funds. But for those that have a reasonable approach to being a bit more active, I think carving out a slice of the pie for that is perfectly acceptable.

Start small as mistakes will be made at first, but over the ensuing 5-10 years, if you have a reasonable active approach, have worked out some kinks, and want to allocate 20/30/40 percent of your savings towards it, there is absolutely nothing wrong with that.

As I mention ad nauseam, the absolute key to investing is finding which strategies align with your goals, personality, and curiosity/knowledge. If you can find that match, you will be successful.

Let me know your thoughts and have fun out there!